Seattle’s current housing prices are a byproduct of our current supply and demand curves. If we affect one or the other, median house prices will change. This is exactly why it’s such great news for the Puget Sound housing market that the Federal Housing Finance Agency (FHFA) increased conforming loan limits to the extent that they did!

The new conforming loan limits are:

King, Pierce and Snohomish Counties: $726,525 (up 8.92% from 2018’s loan limit of $677,000)

Kitsap, Skagit, Island, and Mason Counties: $484,350 (up 6.9% from 2018’s loan limit of $453,100)

Increasing Loan Limits Clear the Way

This increases the purchase price ceiling by 8.9% for many homebuyers. Starting on January 1, preapproved purchase prices for many homebuyers will raise. This will directly impact the demand for homes at higher price points. Ultimately this higher demand will clear the way for home prices to appreciate higher than they otherwise may have, given last year’s conforming loan limits.

Here’s some context: any loan above the conforming loan limit is considered a Jumbo loan. These jumbo loans are not backed by Fannie Mae or Freddie Mac. That means loans above the conforming loan limit are funded by banks’ own dollars. Banks are in business to turn a profit, while Fannie Mae and Freddie Mac were founded to promote homeownership. Additionally, they are currently government-sponsored entities. Given the differences in philosophies, banks’ lending guidelines, or underwriting requirements, for jumbo loans are generally much stricter than the lending guidelines for a Fannie Mae or Freddie Mac home loan. Due to this, many homebuyers’ purchase price ceilings are highly dependent on Fannie Mae and Freddie Mac’s conforming loan limits. So, if those loan limits increase, so does the purchasing power for many homebuyers.

Why Not a Jumbo Loan?

The biggest deterrents for jumbo loans are:

- Higher required credit scores (Fannie and Freddie will approve with scores as low as 620)

- Higher down payment (Fannie and Freddie only require 5% down on loan between $484,350 and $726,525)

- Reserve requirements (This is the amount of liquid cash required to have on hand after closing on the new home…Fannie and Freddie don’t have reserve requirements)

- Tradeline requirements (Oftentimes borrowers are required to have a certain number of tradelines if using a Jumbo loan program)

- Debt to Income Ratios (Fannie and Freddie will go up to 50% DTI…most jumbo loans will only go to 38%, or 43% with some compensating factors)

Because it’s so much harder to get approved for a jumbo loan, many borrowers are capped by the conforming loan limits. For example, previously a homebuyer may have been capped at $846,250 purchase price with 20% down due to not meeting the reserve requirements of a jumbo loan program. This limit was in place regardless of what a homebuyer could afford on a monthly income basis. This move by the FHFA means the homebuyer is now approved for a $908,000 purchase price with 20% down. This results in a $726,400 loan amount – which is now within the conforming loan limits.

Interest Rate Update

Per Bankrate.com, the 30 Year Mortgage interest rate declined 9 basis points this past week to 5.01%, with .33 in discount and origination points. Rates are .93% higher than the 52-week low-interest rate and are near their highest levels since February 2011.

Seattle Inventory Tracker:

Down 5.39% in past week

Down 11.96% since 11.2.18 (1,355 homes for sale in Seattle proper on 11.2.18)

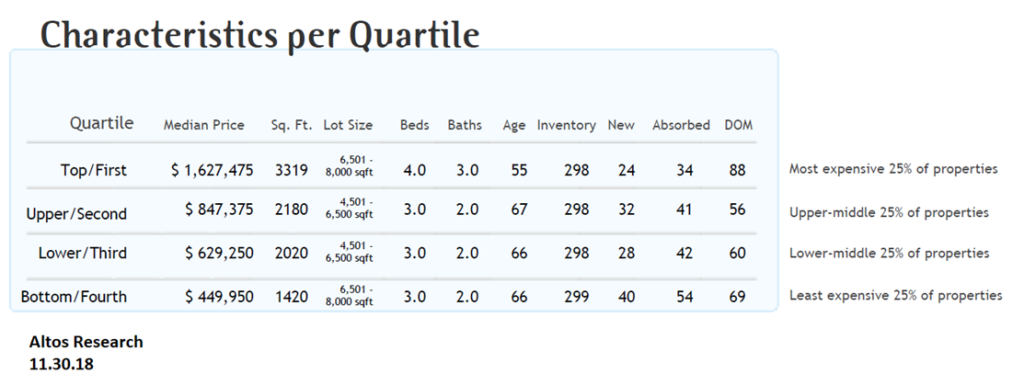

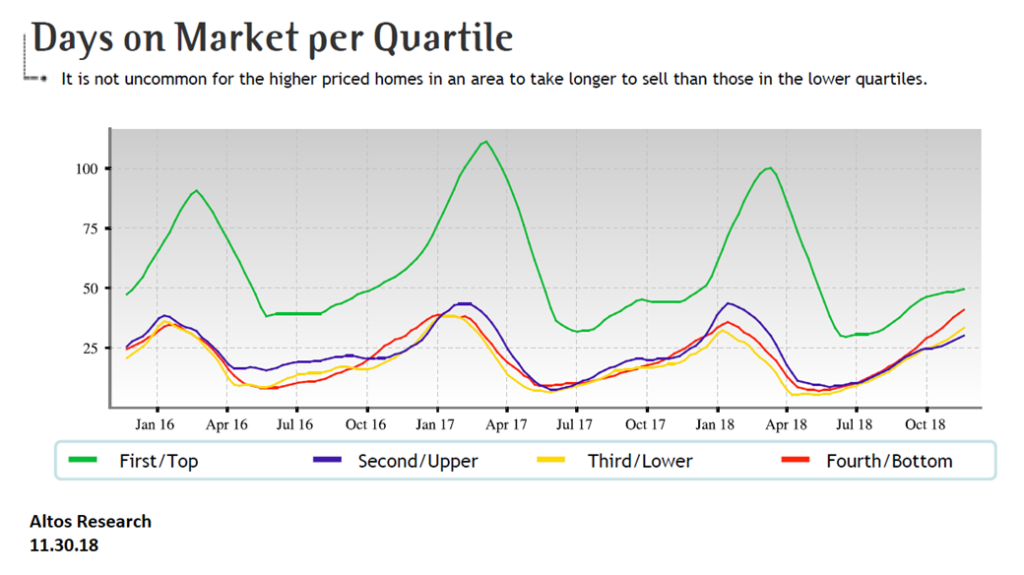

These charts are Seattle Specific, but the Puget Sound Real Estate Market mirrors the Seattle market.

Scott Sheridan is a Loan Officer with Primary Residential Mortgage, Inc. Being in the mortgage industry for three years, Scott brings a fresh millennial flair to the industry. He is well-versed in the most modern, efficient, and convenient ways to get things done. Scott combines these skills with a genuine love of his work and recent experience in what is it like to be a first and second-time home buyer. You can follow Scott’s weekly market updates on his PRMI Facebook Page.

Scott Sheridan is a Loan Officer with Primary Residential Mortgage, Inc. Being in the mortgage industry for three years, Scott brings a fresh millennial flair to the industry. He is well-versed in the most modern, efficient, and convenient ways to get things done. Scott combines these skills with a genuine love of his work and recent experience in what is it like to be a first and second-time home buyer. You can follow Scott’s weekly market updates on his PRMI Facebook Page.

Be First to Comment