The government shutdown finally ended on day 35. But, federal workers just missed their second paycheck. This is the longest government shutdown in history, and many people have asked how or if it’s affecting our local housing market. Well, let’s take a look at some data points:

- This is the longest government shutdown in history. IT lasted 35 days. The second longest government shutdown on record was in December of 1995. That shutdown lasted 21 days.

- The average pay for the government workers affected is about $3,685 per month, or $44,200 per year.

- On top of the 800,000+ government workers, there are about 10,000 businesses that do contract work for the government who aren’t getting paid. All told, it’s about $200,000,000 per week nationally that these contractors are missing out on. But more locally, we’re looking at about $100-$500k in King and Thurston County (Olympia); and $500-$1,000,000 in Pierce County (Joint base Lewis-McChord).

- Washington State has about 16,000 government workers affected. The departments taking the biggest hits are the: Agriculture Department (2,783 employees), Interior Department (2,601), Transportation Department (2,187), Social Security Department (1,382), and Commerce Department (1,130).

- GDP is expected to drop .5% in Q1 of 2019 due to the shutdown if it lasts another week.

What That Means For The Market

If the shutdown continued for much longer, ramifications of the shutdown will start to trickle up. They would eventually affect our local housing market. There are some housing markets which will feel the effects of the shutdown more than others, and sooner. For example, Tacoma and Olympia will feel the effects before Seattle does. Reason being, for one, there’s a higher per capita number of people affected in those areas. But two, the people affected in those areas make up a bigger portion of the home-buying activity since housing prices are more affordable in Tacoma and Olympia than they are in Seattle.

In Seattle, a majority of the home-buying population is not, and has not been government workers who are affected by the shutdown. Therefore the Seattle housing market is not directly affected by the shutdown.

Since long government shutdowns are a reality now, let’s look at the potential impact of the shutdown going longer. Effects of as longer shutdown will trickle up and will affect the Seattle housing market. A couple scenarios: If GDP drops .5%, then that’s usually not great for the stock market, and homebuyers’ saved down payment funds may fall. Another scenario that could play out if the shutdown continued is contractors having to lay off or furlough some (more) of their employees. Though the average government worker at $44,200 per year may not be buying a home in Seattle, employees and owners of businesses who do contract work with the government DO buy homes in Seattle. If those businesses run out of reserves, that would be really bad.

Interest Rates Check-in

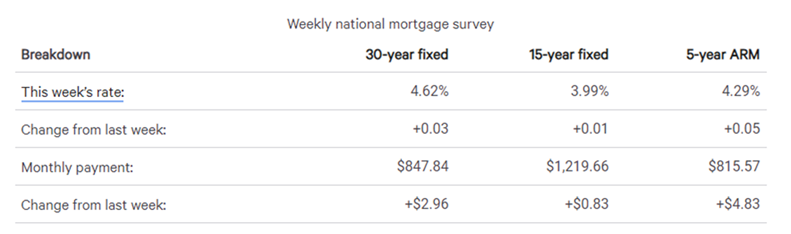

Mortgage rates move higher for the first time in a month. Per Bankrate.com, the 30 Year Mortgage interest rate rose to 3bps to 4.62% with .36 in discount and origination points being charged to the borrower. Rates are still .12% lower than the 52 week average of 4.74%.

Mortgage rates this week

The benchmark 30-year fixed-rate mortgage rose this week to 4.62 percent from 4.59 percent, according to Bankrate’s weekly survey of large lenders. A year ago, it was 4.27 percent. Four weeks ago, the rate was 4.75 percent. The 30-year fixed-rate average for this week is 0.48 percentage points below the 52-week high of 5.10 percent and is 0.24 percentage points above the 52-week low of 4.38 percent.

The 30-year fixed mortgages in this week’s survey had an average total of 0.36 discount and origination points.

Over the past 52 weeks, the 30-year fixed has averaged 4.74 percent. This week’s rate is 0.12 percentage points lower than the 52-week average.

- The 15-year fixed-rate mortgage rose to 3.99 percent from 3.98 percent.

- The 5/1 adjustable-rate mortgage rose to 4.29 percent from 4.24 percent.

- The 30-year fixed-rate jumbo mortgage rose to 4.60 percent from 4.56 percent.

- At the current 30-year fixed rate, you’ll pay $513.84 each month for every $100,000 you borrow, up from $512.05 last week.

- At the current 15-year fixed rate, you’ll pay $739.19 each month for every $100,000 you borrow, up from $738.69 last week.

- At the current 5/1 ARM rate, you’ll pay $494.28 each month for every $100,000 you borrow, up from $491.35 last week.

Results of Bankrate.com’s weekly national survey of large lenders conducted January 23, 2019 , and the effect on monthly payments for a $165,000 loan:

The “Bankrate.com National Average,” or “national survey of large lenders,” is conducted weekly. The results of this survey are quoted in our weekly articles and national media outlets. To conduct the National Average survey, Bankrate obtains rate information from the 10 largest banks and thrifts in 10 large U.S. markets. In the Bankrate.com national survey, our Market Analysis team gathers rates and/or yields on banking deposits, loans and mortgages. We’ve conducted this survey in the same manner for more than 30 years, and because it’s consistently done the way it is, it gives an accurate national apples-to-apples comparison. https://www.bankrate.com/mortgages/analysis/

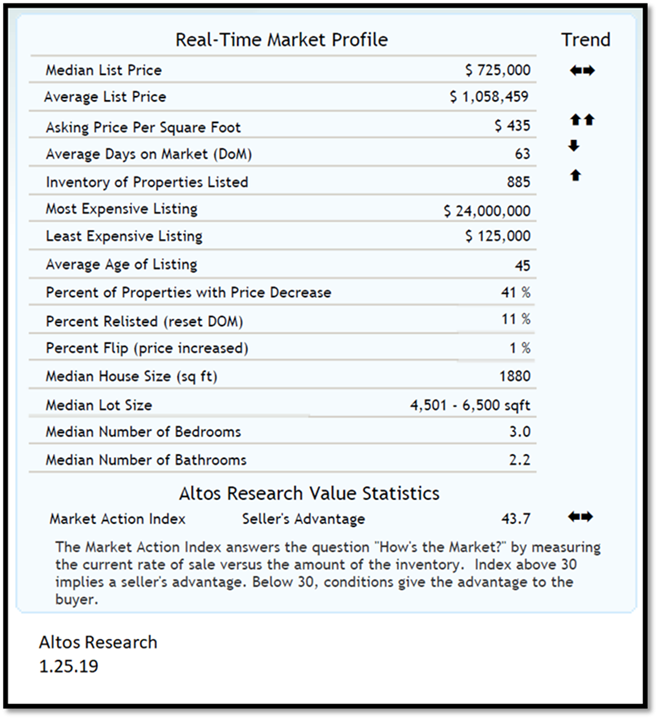

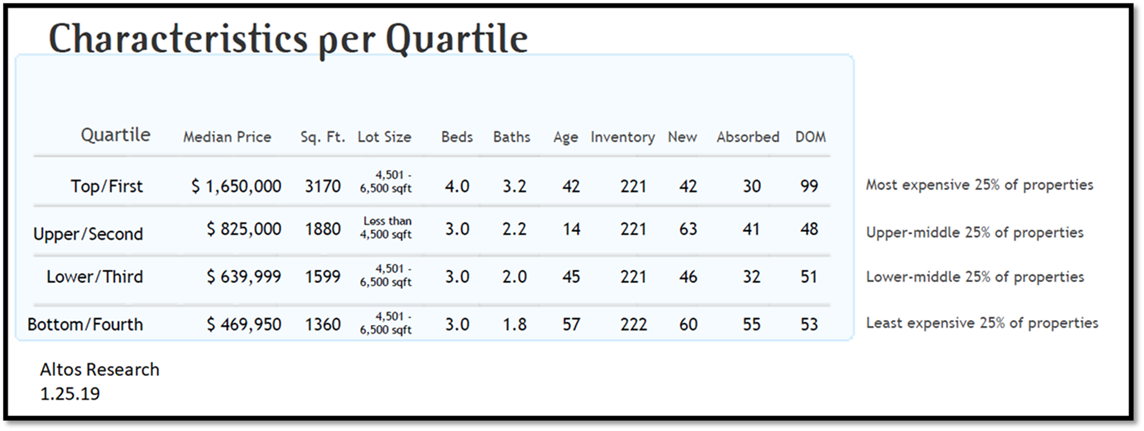

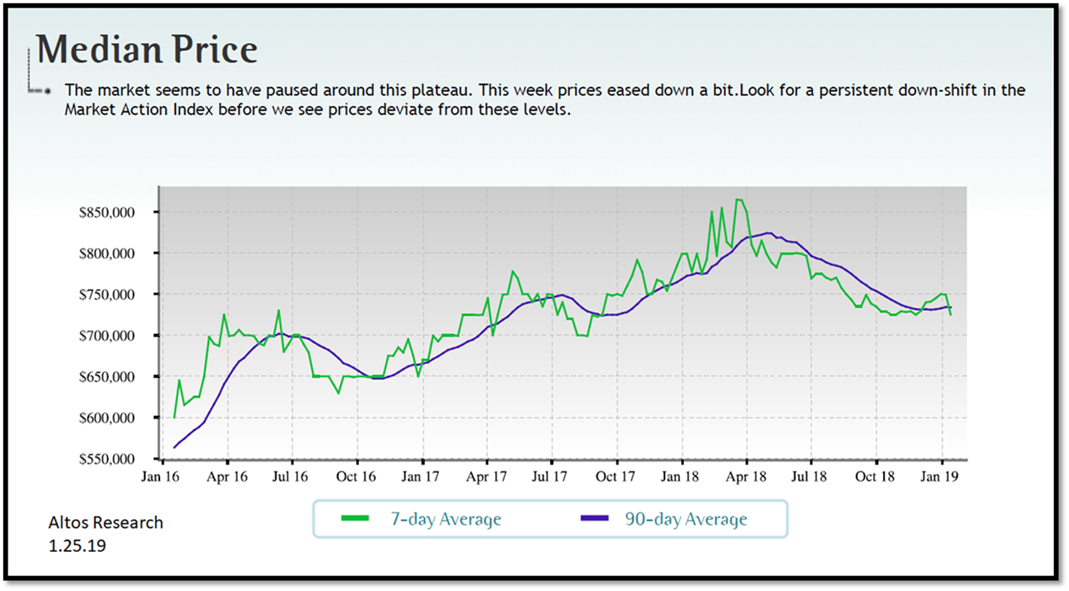

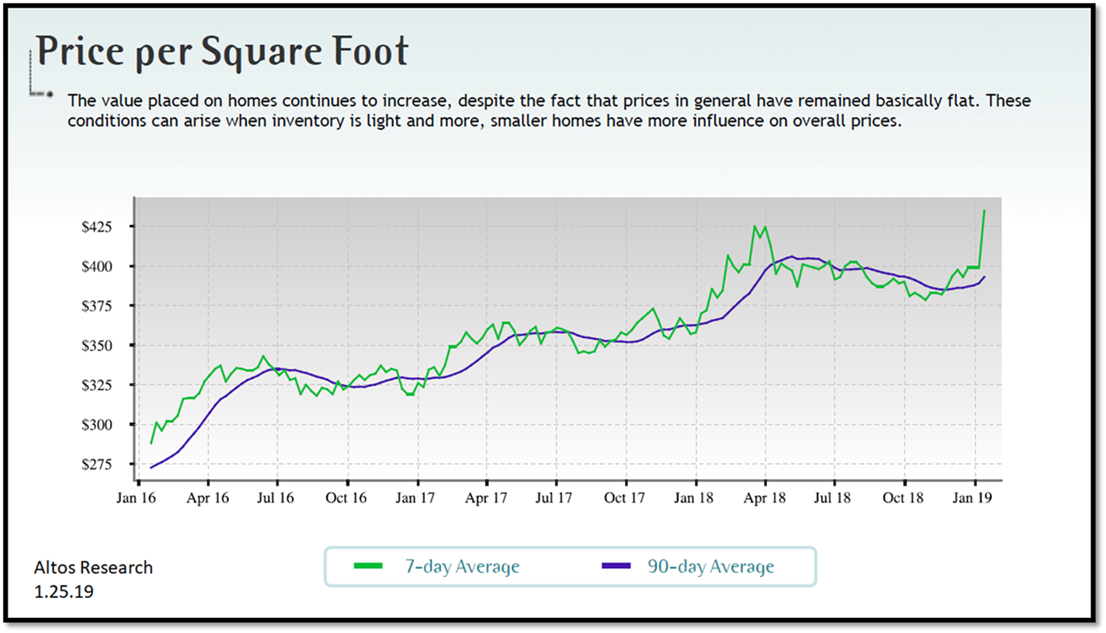

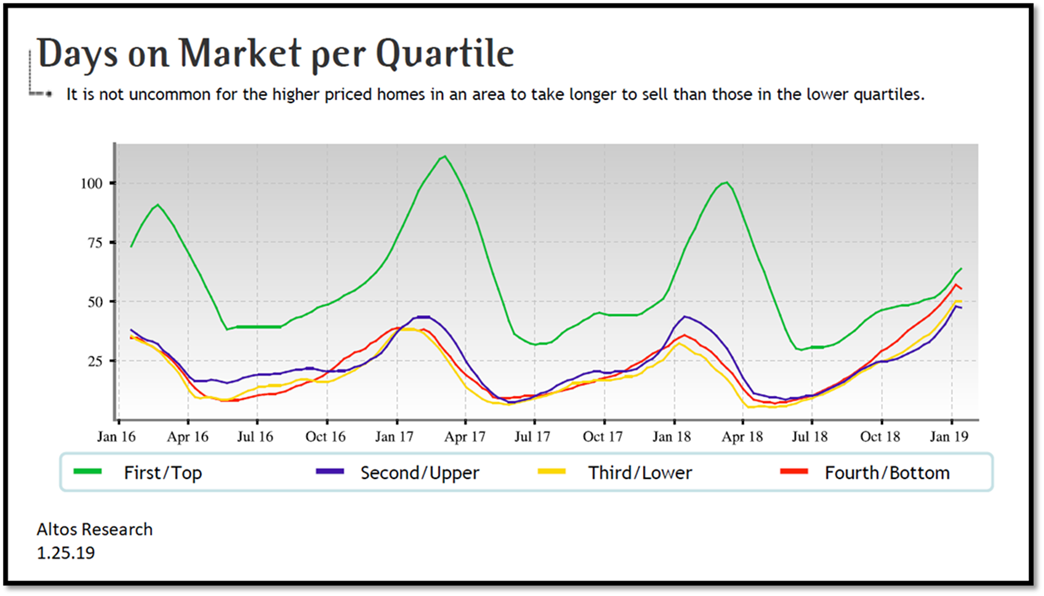

City of Seattle Stats for Single Family Residences – 1.25.19

Please note, the data in the charts below does not make a lot of sense, leading me to believe there may have been an error when Altos Research compiled the data. For example, I don’t think the median house price fell $25,000 last week; alongside price per square foot rising 9.02%. That doesn’t make sense… I also don’t think inventory jumped 30% in one week (in January, no less). I will be curious to see what Altos’ data looks like next week and if some of the datapoints fall back in-line with the overall trend lines.

These charts are Seattle Specific, but the Puget Sound Real Estate Market mirrors the Seattle market.

Scott Sheridan is a Loan Officer with Primary Residential Mortgage, Inc. Being in the mortgage industry for three years, Scott brings a fresh millennial flair to the industry. He is well-versed in the most modern, efficient, and convenient ways to get things done. Scott combines these skills with a genuine love of his work and recent experience in what is it like to be a first and second-time home buyer. You can follow Scott’s weekly market updates on his PRMI Facebook Page.

Be First to Comment