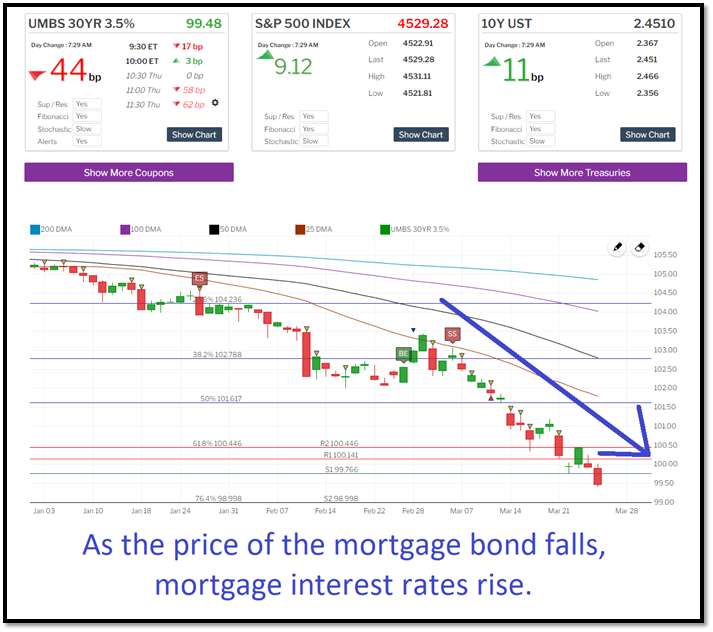

For the past two years we’ve seen amazing mortgage interest rates. Those rates are about to become a fond memory. The primary reason mortgage interest rates are skyrocketing right now is investment managers are scrambling to preserve their capital.

As of 2021, the University of Washington had a $4.88 billion endowment. Unsurprisingly, that endowment is essential to funding the everyday operations of the University. For example, in 2017 the University reported $443,383,000 of investment income derived from the endowment. Most of those endowment funds are held in equity investments, like the stock market. Some of this equity is in Real Estate, but another big chunk is held in Fixed Income investments. What exactly is a Fixed Income Investment? It’s an investment approach focused on the preservation of capital. It typically includes investments like government and corporate bonds, CDs and money market funds, and Mortgage Backed Securities (MBS).

Like all other investment managers, those at the University of Washington Endowment are working overtime to preserve the endowment’s capital.

One part of preserving capital is simply not to lose it. But the other, and most important part of preserving capital is preserving its spending power. Remember when you could buy a Coke at a vending machine for a $1? Now it’s oftentimes $1.50 (if not more). If I had $100 in 1995 and wanted to ensure I could continue buying 100 Cokes any time I wanted, I would need to have invested my $100 somewhere that could keep up with the rising cost of Coke. If I hadn’t invested that money somewhere and simply threw it under my mattress instead, sure – I’d still have a $100 bill, but I’d only be able to buy 67 Cokes at today’s $1.50 per Coke. I would have preserved the capital in the sense that I didn’t lose my $100 bill, but I would’ve NOT preserved it in the sense that it doesn’t buy me 100 Cokes like it used to.

This story highlights the primary reason investment managers don’t throw money under their mattresses, but rather invest that money in extremely secure investments that pay out a small fixed return – to keep ahead of the rising costs of goods and to preserve the spending power of their capital.

The rising cost of goods is called inflation.

For the past 10 years, inflation has hung around 2%. Relatively stable inflation at about 2% means that investment managers are comfortable buying Fixed Income Assets like mortgage bonds at 3%. After all, that manager is preserving the capital by putting it into an extremely safe investment, but also earning a return large enough to actually keep ahead of inflation and thereby preserving their capital’s spending power as well. Said another way, that investment manager is netting a 1% return on their investment. But when inflation skyrockets from 2% to 7.9%, all of a sudden that investment manager doesn’t like their 3% mortgage bonds anymore.

Some of the reasons for the jump in inflation are:

- Supply chain bottlenecks due to COVID shutdowns

- Wage growth as businesses attempt to attract good workers (as we come out of COVID)

- And now soaring commodity prices like oil, wheat, and nickel due to the Russian invasion of Ukraine

After netting a 1% return for the past decade, now they’re LOSING 4.9% due to the increased inflation rates. So they stop buying 3% Mortgage Bonds and start buying [for example] 5% mortgage bonds.

This is why mortgage interest rates are rising so fast. Because inflation is rising so fast. And because investment managers are no longer buying low-yield mortgage bonds. They want higher yield ones to keep up with rising inflation.

Summary

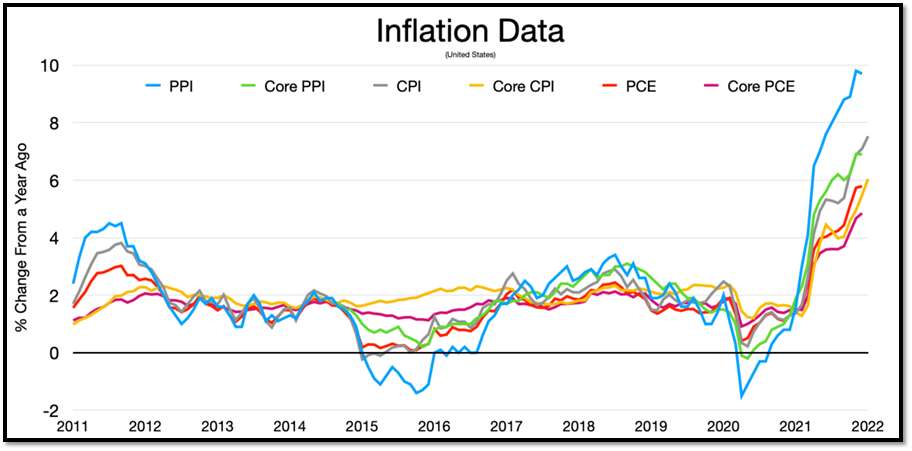

Every inflation metric we have shows inflation rates shooting for the moon.

- The Producer Price Index (PPI – measures the wholesale cost of goods to producers)

- Core PPI (which is the PPI but stripping out volatile out food and energy variables)

- Consumer Price Index (CPI – measures the cost of goods to consumers – data sourced from consumers)

- Core CPI (which is the CPI but again, stripping out volatile food and energy variables)

- Personal Consumption Expenditure (PCE – measures the cost of goods to consumers – data sourced from businesses)

- Core PCE (which is the PCE, but stripping out volatile food and energy variables)

The chart below shows all the varying rates rising, quickly. Because inflation is skyrocketing, money is flowing out of low-yield mortgage bonds and into higher-yield mortgage bonds, thus driving up mortgage interest rates.

Eventually, this will end, but with Russia continuing its invasion and China and other parts of Asia shutting down due to Omicron2, the world economy is stuck in a vortex of increasing inflation until one of the three variables above can turn it around.

Interest

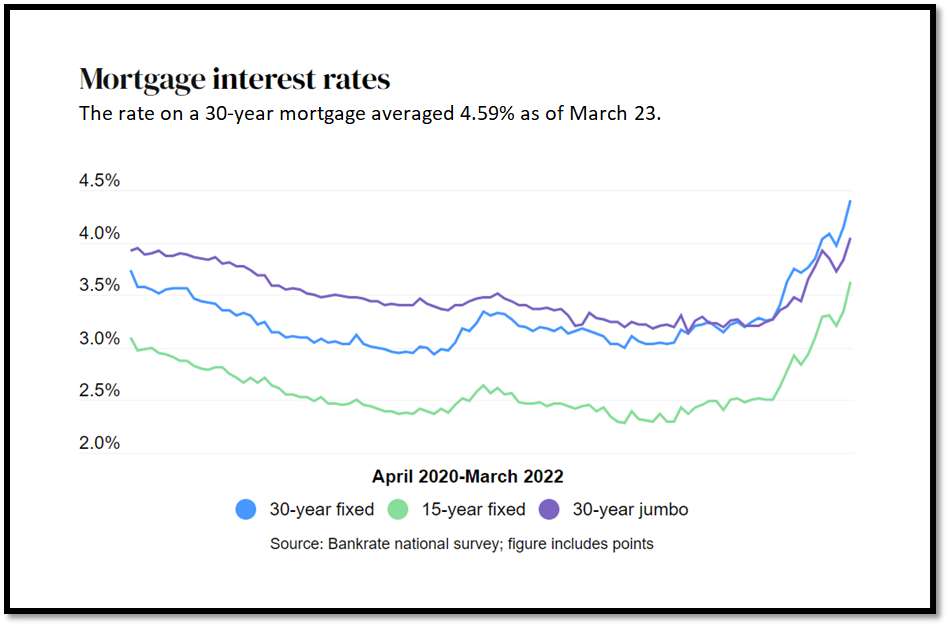

Per Bankrate’s survey of large lenders, the 30-year mortgage interest rate rose this past week to 4.59%, with .32 in discount and origination points.

Mortgage Market Week in Review

See above. Things are likely to get worse before they get better.

What you need to know for where rates will go:

- Good Economic News or Inflation = Bad for Mortgage Interest Rates.

- Bad Economic News or Deflation = Good for Mortgage Interest Rates.

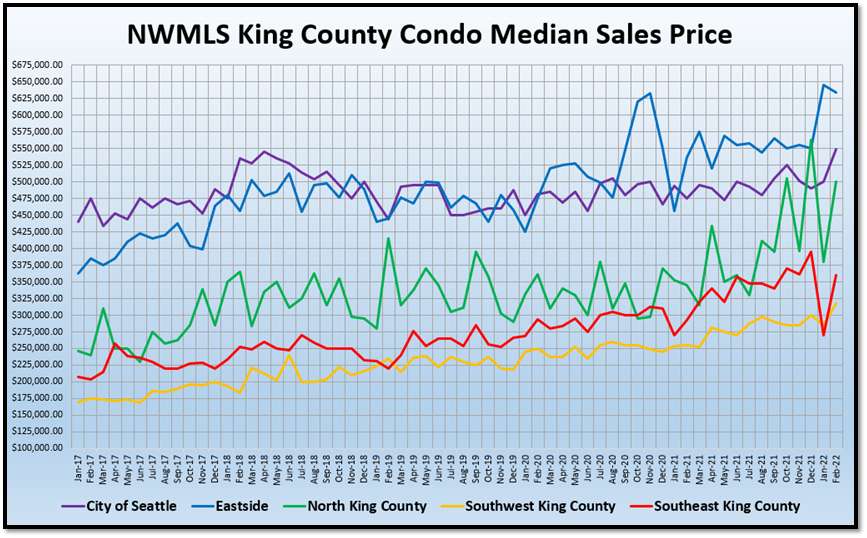

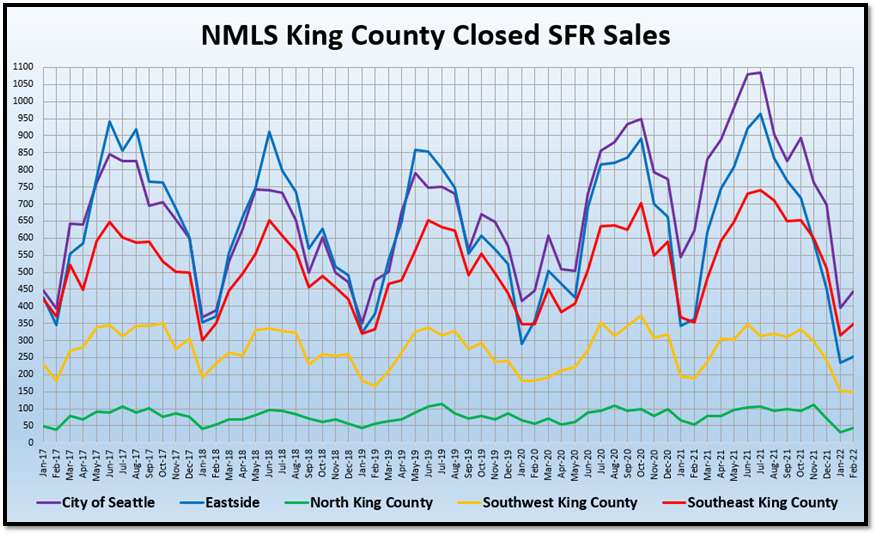

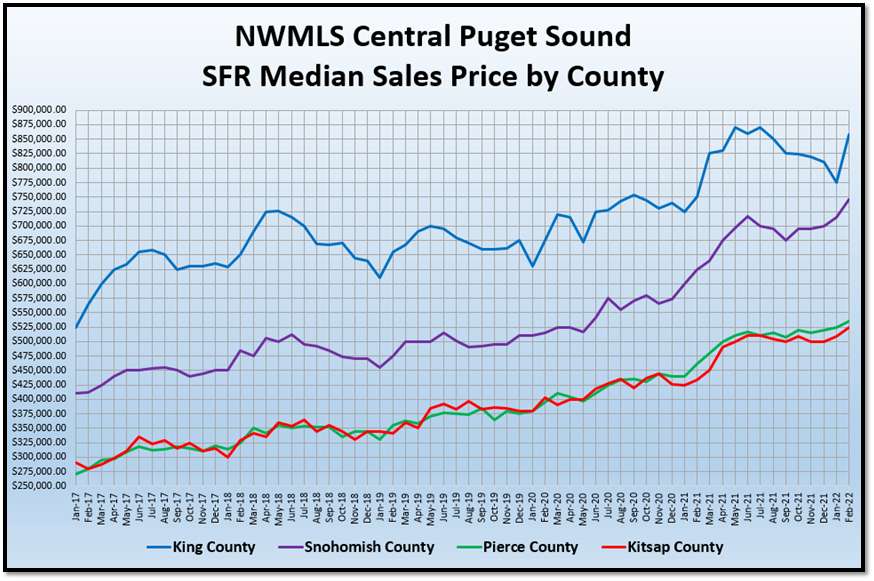

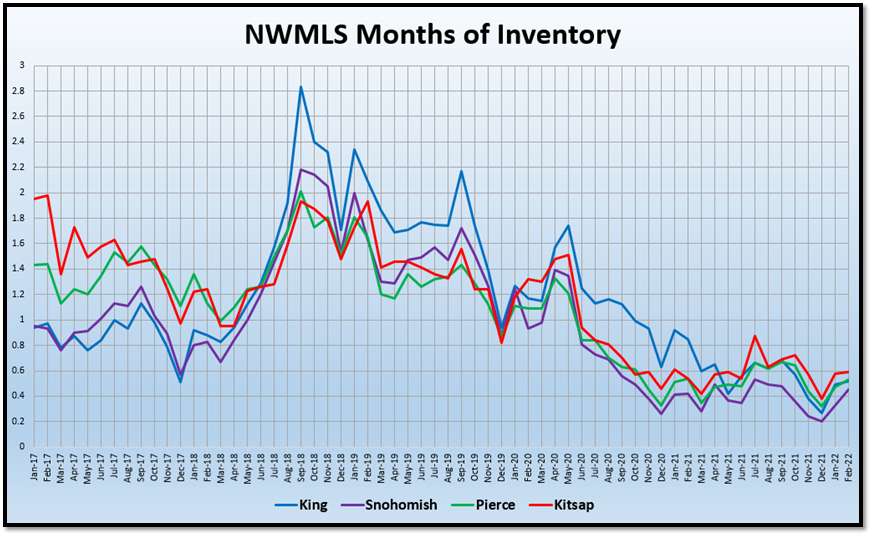

Puget Sound Real Estate: Charts and Data

Absorption Rates per NWMLS 3.15.22

Absorption Rate is calculated as: (Pending Sales) / (Active + Pending Sales)

Residential in Seattle: 72.33%

Condos in Seattle: 53.93%

Residential in Bellevue/Redmond/Kirkland: 79.84%

Condos in Bellevue/Redmond/Kirkland: 76.59%

Residential in Everett/Marysville/Lake Stevens: 83.76%

Condos in Everett/Marysville/Lake Stevens: 87.36%

Residential in Tacoma/Lakewood/Federal Way: 72.75%

Condos in Tacoma/Lakewood/Federal Way: 69.64%

Scott Sheridan is a Loan Officer with Primary Residential Mortgage, Inc. Scott brings a fresh millennial flair to the industry, shown through his innovative ideas and future-thinking solutions throughout his years in the mortgage industry. He is well-versed in the most modern, efficient, and convenient ways to get things done. Scott combines these skills with a genuine love of his work and recent experience in what is it like to be a first and second-time home buyer.

Be First to Comment