Due to the economics of scarcity, housing prices are soaring across Western Washington. That has many of us worried about the sustainability of our current market. To be fair, 15%+ year over year appreciation growth is NOT sustainable if it happened every year for years and years on end. But before throwing your hands up and declaring THIS market a bubble that’s bound to pop, let’s investigate What’s Possible?

A Benchmark to the South

Luckily for us, we have a near-perfect comparable city to benchmark off of about 850 miles to the south: San Francisco.

For as long as I can remember, San Francisco has consistently been about 10 years ahead of us. Check this out: In January of 2011, the median price of a home in San Francisco County was about $750,000. In January of 2021, the median price of a home in King County was about $725,000. Not exact, but pretty darn close.

The reality is, San Francisco has a similar economy to ours (mostly rooted in Tech), similar geographical boundaries restricting available buildable land (Ocean on one side, big bay on the other), and both have a generally highly educated and politically left-leaning population. At the end of the day, the biggest difference between Seattle and San Francisco is, again, that they’re about 10 years further down the road than us.

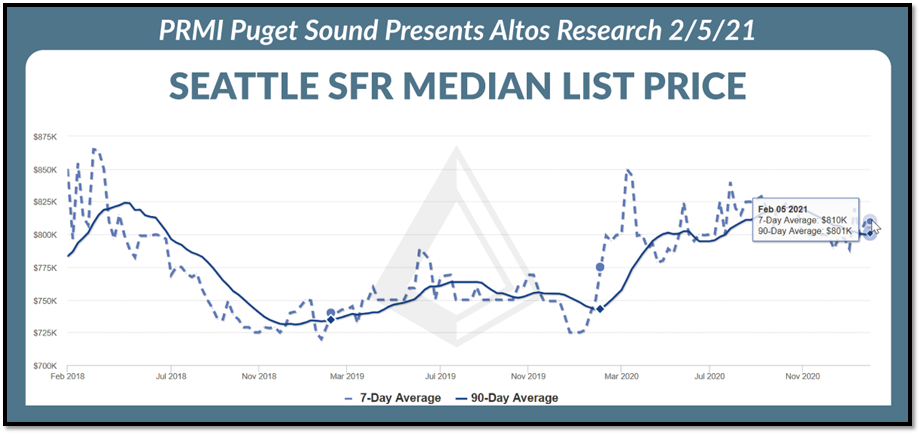

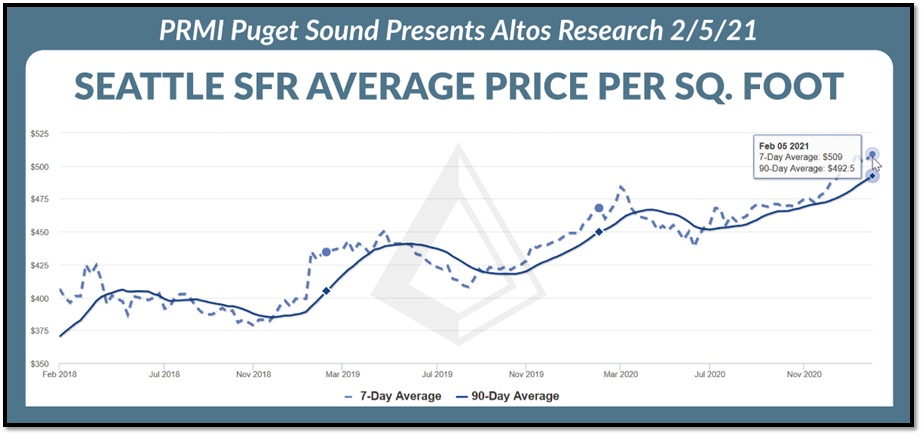

So given the similarities between cities, we have the opportunity to project what Seattle’s future might look like based on what things look like down in SFO. So how are things looking down there? According to Altos Research, their median SFR price is about $1.5m right now, and price per square foot is $954. Seattle’s median SFR price right now is about $810,000 with a price per square foot of $509. So for as unsustainable and ridiculous as OUR market might seem, we are a 45% off clearance sale compared to San Francisco.

Summary

Since 2015 I’ve been hearing that our PNW housing market is unsustainable. However, according to the NWMLS, the median list price for a home (house and condo) in King County in January of 2015 was $400,000…and now the NWMLS has King County at $644,950…a 61% increase in the last 5 years. The thing with declaring something unsustainable is that it’s all relative. Again, 15%+ year over year appreciation growth is NOT sustainable if it happened every year for years and years on end. But to declare our current market unsustainable based on price and perceived affordability? Ya might just wanna look 850 miles to the south to see What’s Possible, and what the future might hold for Seattle’s housing market.

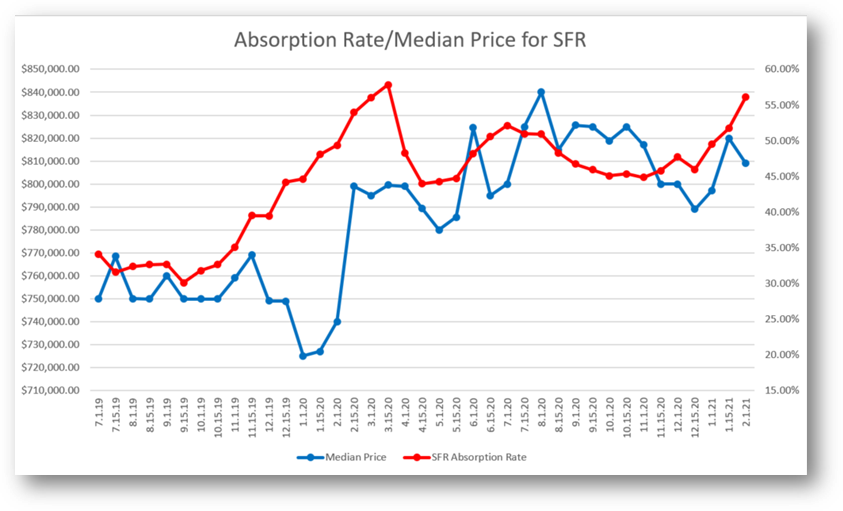

Alex Black Absorption Rates per NWMLS Real-Time Data

Absorption Rate is calculated as: (Pending Sales) / (Active + Pending Sales)

SFR in Seattle

- SFR Pending Sales in Seattle: 841 homes

- SFR Active Listings in Seattle: 488 homes

- Absorption Rate for SFR in Seattle: 63.28%

- Don’t let the declining median house price catch you. Make no mistake about it: At an all-time high absorption rate for SFR in Seattle, THIS IS A SELLERS MARKET. Chalk the overall declining median LIST price up to new sellers wanting to sell fast and entice buyers with below market pricing. But as all of us in the industry know, this declining median list price is temporary, and ultimately escalation clauses between competing buyers will drive prices higher.

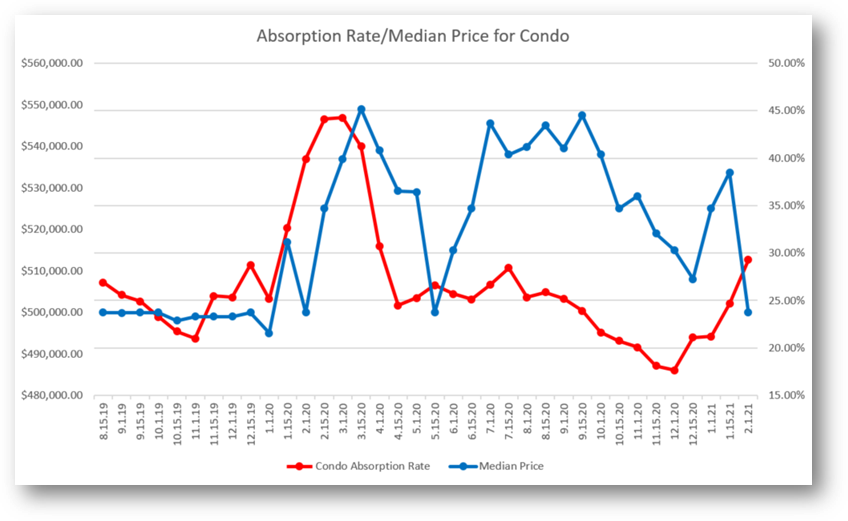

Condos in Seattle

Condos in Seattle

- Condo Pending Sales in Seattle: 289 condos

- Condo Active Listings in Seattle: 572 condos

- Absorption Rate for Condos in Seattle: 33.57%

- Similar to SFR, don’t let the declining median LIST price fool ya. The absorption rate for condos in the city is DOUBLE what it was when we entered December, and the reality is the price per square foot is up 2.8% since December 1…implying that the main reason the median list price is down is because the average size of condo on the market right now is simply smaller than it was at the beginning of December.

Interest Rates

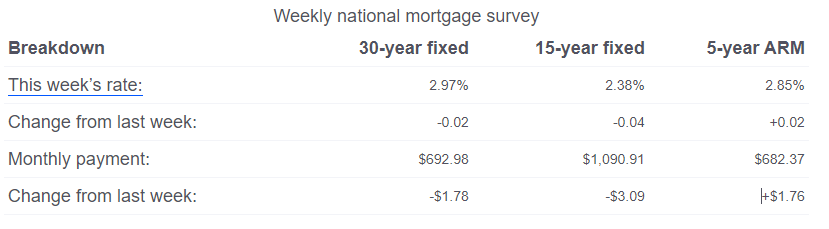

Per Bankrate.com’s survey of large lenders, the 30-year mortgage interest rate fell slightly this past week to 2.97%, with .32 in discount and origination points.

According to Bankrate, rates have fallen .91% since their 52-week high of 3.88%

(That’s a savings of $252.68 per month on a $500,000 loan!)

Mortgage rates this week

The benchmark 30-year fixed-rate mortgage fell this week to 2.97% from 2.99%, according to Bankrate’s weekly survey of large lenders.

A year ago, it was 3.71%. Four weeks ago, the rate was 3.01%. The 30-year fixed-rate average for this week is 0.91 percentage points below the 52-week high of 3.88%, and is 0.04 percentage points above the 52-week low of 2.93%.

The 30-year fixed mortgages in this week’s survey had an average total of 0.32 discount and origination points.

Over the past 52 weeks, the 30-year fixed has averaged 3.28%. This week’s rate is 0.31 percentage points lower than the 52-week average.

- The 15-year fixed-rate mortgage fell to 2.38% from 2.42%.

- The 5/1 adjustable-rate mortgage rose to 2.85% from 2.83%.

- The 30-year fixed-rate jumbo mortgage fell to 3.36% from 3.37%.

- At the current 30-year fixed rate, you’ll pay $419.99 each month for every $100,000 you borrow, down from $421.06 last week.

- At the current 15-year fixed rate, you’ll pay $661.16 each month for every $100,000 you borrow, down from $663.03 last week.

- At the current 5/1 ARM rate, you’ll pay $413.56 each month for every $100,000 you borrow, up from $412.49 last week.

Results of Bankrate.com’s weekly national survey of large lenders conducted February 10, 2021 and the effect on monthly payments for a $165,000 loan:

Where mortgage rates are headed

Mortgage experts were mixed on rate trend predictions in Bankrate’s survey this week (Feb. 10-Feb. 17). In response to Bankrate’s weekly poll, 46% said rates will stay more or less the same next week and 38% said they would rise. Meanwhile, 15% said next week mortgage rates will decline.

“With the 10-year Treasury heading toward 1.20 and a massive stimulus package on the way I would expect rates to inch higher this week. This could very well be short term in nature as I also expect the markets to deal with uncertainty regarding reopening and the annual inflation fear discussion we seem to get every year,” said Gordon Miller, owner, Miller Lending Group, LLC, Cary, North Carolina.

Now is the right time for a refinance

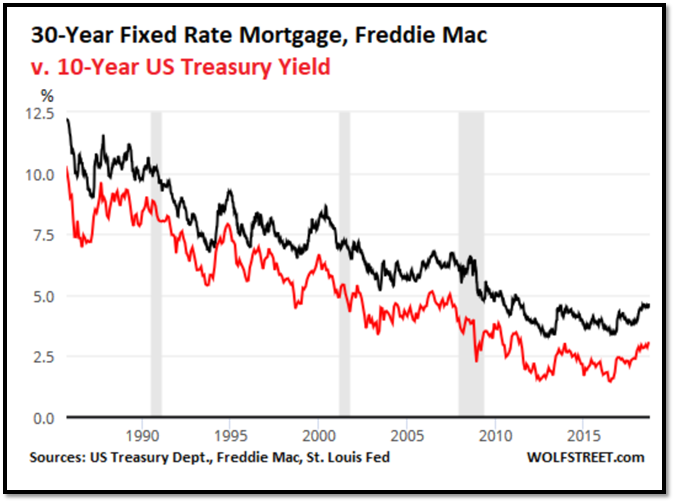

Rates are just above a record low, but they might be going up soon. The rate on 10-year bonds issued by the U.S. government has stayed above 1% for a month now. The 10-year Treasury is closely tied to 30-year mortgage rates.

Even if you don’t own 10-year Treasury notes, the rate on the benchmark bonds still can affect how much you pay for your mortgage. The 10-year Treasury acts as a reliable indicator of economic sentiment and as a key benchmark for mortgage rates. In 2019, the gap between the 10-year Treasury and the 30-year mortgage averaged 1.79 points, according to a Bankrate analysis of data compiled by the Federal Reserve Bank of St. Louis.

A year ago, the rate on the 10-year Treasury was north of 1.9%. Then the coronavirus pandemic hit, and rates on 10-year bonds plummeted. The 10-year rate fell as low as 0.52% in August.

The bottom line: It may be time to do that refinance sooner rather than later.

The Bankrate.com national survey of large lenders is conducted weekly. To conduct the National Average survey, Bankrate obtains rate information from the 10 largest banks and thrifts in 10 large U.S. markets. In the Bankrate.com national survey, our Market Analysis team gathers rates and/or yields on banking deposits, loans and mortgages. We’ve conducted this survey in the same manner for more than 30 years, and because it’s consistently done the way it is, it gives an accurate national apples-to-apples comparison. Our rates may differ from other national surveys, in particular Freddie Mac’s weekly published rates. Each week Freddie Mac surveys lenders on the rates and points based on first-lien prime conventional conforming home purchase mortgages with a loan-to-value of 80 percent. “Lenders surveyed each week are a mix of lender types – thrifts, credit unions, commercial banks and mortgage lending companies – is roughly proportional to the level of mortgage business that each type commands nationwide,” according to Freddie Mac.

https://www.bankrate.com/mortgages/analysis/

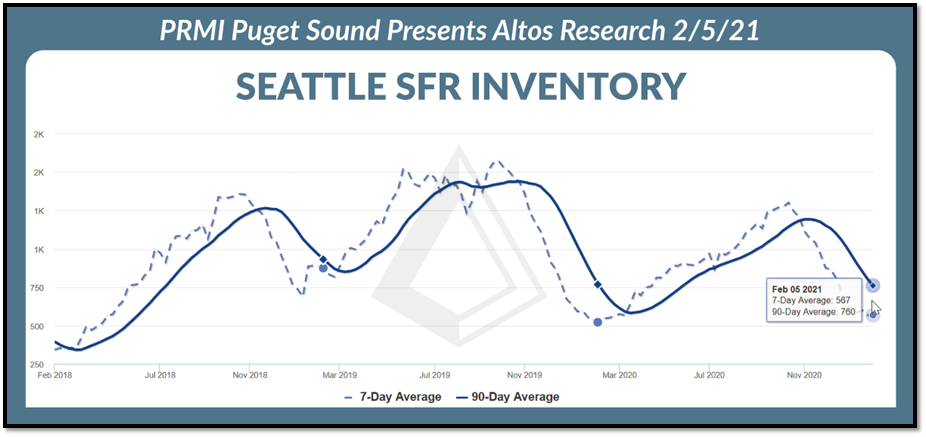

The charts in this article are Seattle Specific, but Puget Sound Real Estate mirrors the Seattle market.

Scott Sheridan is a Loan Officer with Primary Residential Mortgage, Inc. Being in the mortgage industry for four years, Scott brings a fresh millennial flair to the industry. He is well-versed in the most modern, efficient, and convenient ways to get things done. Scott combines these skills with a genuine love of his work and recent experience in what is it like to be a first and second-time home buyer.

Be First to Comment