It’s been a brutal start to the year for mortgage interest rates. Overall, since the first trading day of 2022 the Mortgage Bond has lost 335bps; which has rates skyrocketing. More recently, since last Monday the Mortgage Bond has lost 118bps. Said another way, Bankrate’s Weekly Interest Rate Survey has climbed to 3.85% with .39 in points on a 30 year fixed rate mortgage from 3.4% and .33 in points at the beginning of the year… And that doesn’t even account for this week’s steep selloff.

Why are rates doing this?

The Fed got the Snowball moving late last year by announcing that they were going to begin curtailing their purchases of mortgage backed securities and treasury bonds. Throughout the Pandemic, the Fed purchased mortgage bonds and treasury bills to create artificial demand for these assets, which drove interest rates and TBills to historic lows. The theory is that if money is cheap, people and businesses will spend more, and therefore soften any potential blows to the stock market and economy. Honestly, it worked! The stock market rose throughout the Pandemic as homeowners were able to save money on their mortgages, and then spend that savings! Unfortunately it may have worked a little too well, as now we have massive supply chain shortages causing high inflation.

As inflation is now at a new 40 year high (7.5% – not seen since 1982), investors are looking at their 3% mortgage bond coupons and thinking to themselves “So the Fed is winding down their purchases of mortgage bonds which has the price of the bond falling, AND I’m only making a 3% return when inflation is 7.5%? I’m selling out in favor of higher yield mortgage bonds.”

Lastly, employees are starting to return to the labor markets, which is really good for the overall economy. So we have some good economic news, which had money flowing out of the lower risk/lower return bond market and into the higher risk/higher return stock market.

Check this out from Elliot Eisenberg:

January employment grew by a strong 467,000. Moreover, December’s employment was revised up from 199,000 to 510,000 and November’s from 249,000 to 647,000, suggesting Omicron had little impact. Better yet, the labor force participation rate rose from 61.9% to 62.2% which had the unemployment rate rise to 4% from 3.9% as workers returned from the sidelines. Wages rose 5.7% Y-o-Y, matching the inflation rate.

That’s some pretty darn good economic news, if you ask me!

Summary

With good economic news, rising inflation, and the Fed reducing their purchasing velocity of mortgage-backed securities; part of me can’t believe things aren’t worse! Mortgage interest rates will probably get worse before they get better, BUT the Fed taking a much more hawkish approach to increasing the Federal Funds Rate faster than expected to ward off further inflation could be good news for mortgage interest rates later this spring and summer. The reason for this is because when the Federal Funds Rate rises, it puts the brakes on the economy, and corporate earnings fall which has money flowing from the high risk/high return stock market and into the lower risk/lower return bond market. Pair that with the idea that inflation should start falling as supply bottlenecks ease with more employees returning to the labor force and year over year inflation benchmarks rising, and we could be in for slightly declining mortgage interest rates later this spring or summer. As always, we shall see; but I’m halfway optimistic that the sky won’t entirely fall on us.

Real Estate Round-Up

For the week of 02/11

Interest Rates

Per Bankrate’s survey of large lenders, the 30-year mortgage interest rate fell this past week to 3.85%, with .39 in discount and origination points.

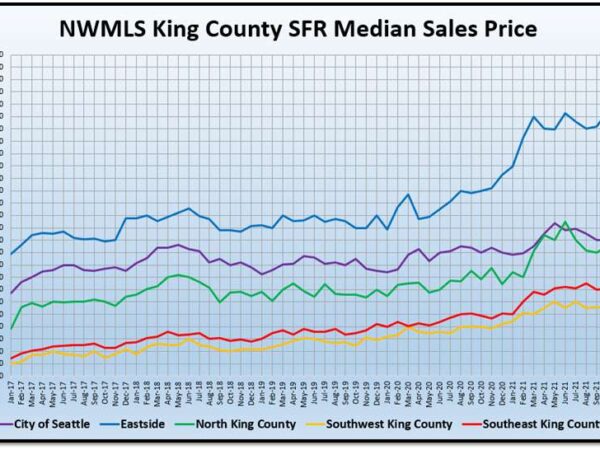

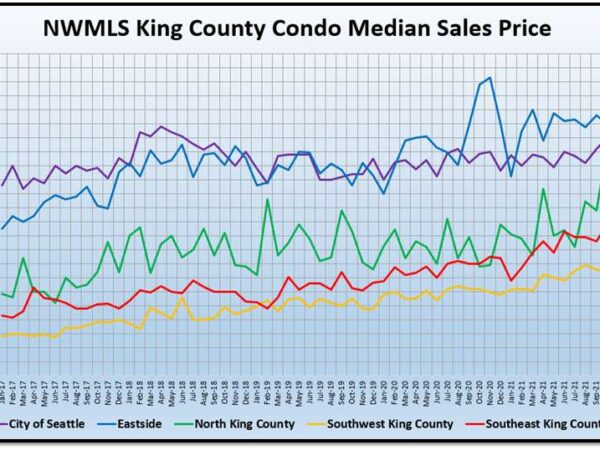

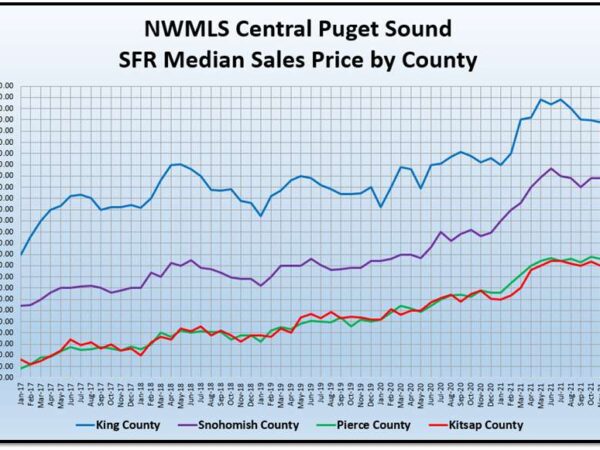

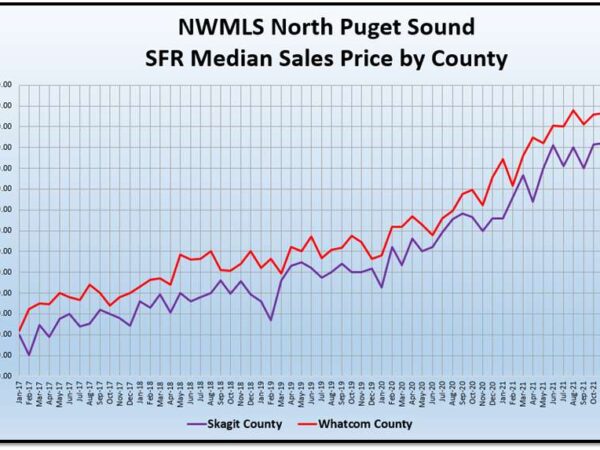

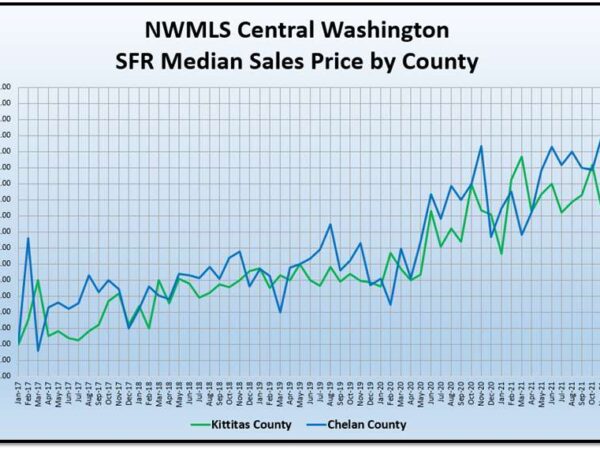

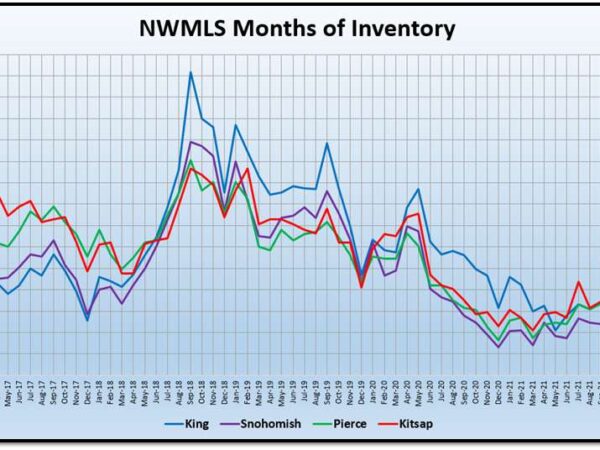

Puget Sound Real Estate: Charts and Data

A picture is worth a thousand words…

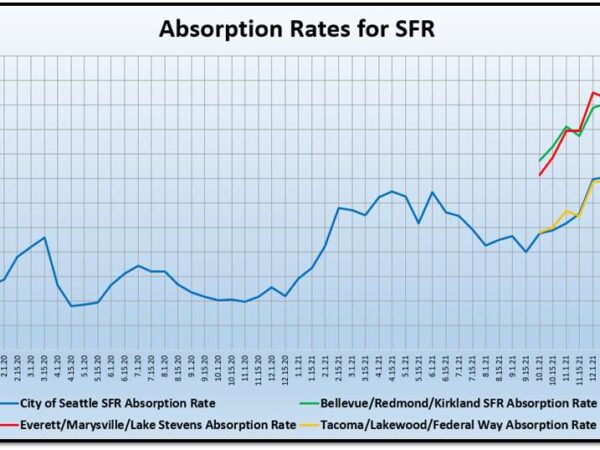

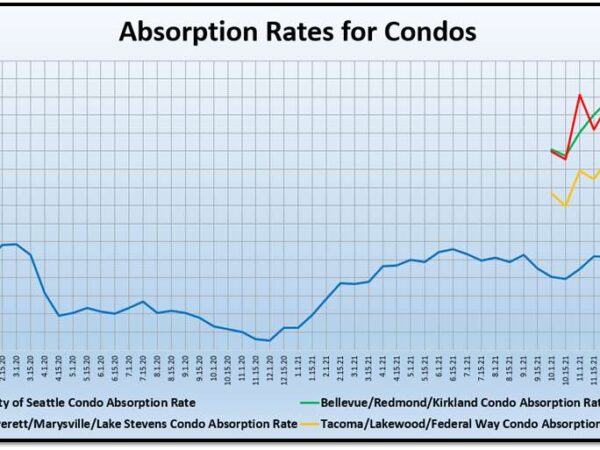

Absorption Rates per NWMLS

Absorption Rate is calculated as (Pending Sales) / (Active + Pending Sales).

Residential in Seattle: 72.25%

Condos in Seattle: 58.14%

Residential in Bellevue/Redmond/Kirkland: 75.57%

Condos in Bellevue/Redmond/Kirkland: 73.58%

Residential in Everett/Marysville/Lake Stevens: 82.37%

Condos in Everett/Marysville/Lake Stevens: 94.87%

Residential in Tacoma/Lakewood/Federal Way: 73.35%

Condos in Tacoma/Lakewood/Federal Way: 67.59%

Scott Sheridan is a Loan Officer with Primary Residential Mortgage, Inc. Scott brings a fresh millennial flair to the industry, shown through his innovative ideas and future-thinking solutions throughout his years in the mortgage industry. He is well-versed in the most modern, efficient, and convenient ways to get things done. Scott combines these skills with a genuine love of his work and recent experience in what is it like to be a first and second-time home buyer.

Be First to Comment