A really fun article came out in the Seattle Times a couple of weeks ago discussing the differences between the Puget Sound housing market Baby Boomers purchased into, compared to the housing market Millennials are now faced with. The Times’ premise is that it’s harder now to purchase than it was then, but I don’t know if I necessarily agree with that.

Let’s dig in

In 1980, the median home price in King County was the equivalent of about $225,000, after adjusting for inflation. Per the latest NWMLS data, the median price of a home in King County is now $625,000. BUT HANG ON! The average interest rate in January 1980 per Freddie Mac was 12.88%, and the average interest rate in August 2019 per Freddie Mac was 3.62% (with .5 points/fees added to closing costs). Thus, after accounting for median house price, inflation, and interest rates, the average P&I payment in 1980 in today’s dollars was $2,467.86, and the average P&I payment in 2019 is $2,848.56. Meaning today’s Millennials are only paying $380.70 more per month than the Boomers did in 1980, not bad!

We need to account for debts and incomes, right? That must be why everyone says it’s harder for Millennials to purchase a home than Boomers. After all, affordability does not only account for the price of the home (which actually isn’t too different for today’s Millennials than it was for the 1980 Boomers as we saw above), affordability is also rooted in debts and income.

Comparing Debts and Income

Let’s start with income. According to the Department of Numbers, the latest data available tells us that the median household income in 2017 for the Seattle metro area was $82,133. According to the US Census, in 1989 (sorry, they didn’t have easily translatable 1980 income data) the Seattle metropolitan area’s median household income was $36,127, or $71,415.85 in today’s dollars after accounting for inflation. After accounting for median house prices and household incomes adjusted for inflation, and factoring in average interest rates, Boomers spent about 41.5% of their annual income on housing, and Millennials are spending about 41.6% of their annual income on housing.

So, it has to be debts then, right? That’s the only reason left for why the narrative of millennial home buying is so much harder than Boomer home buying. Well, the biggest thing that we Millennials complain about is how much school cost, and how school loans got us down. But did you know the average tuition at a public institution in 1980 was $2,550 per year ($8,035.56 in today’s dollars)? Compared to the current annual cost of attendance at the University of Washington of $10,974 per year. True, that’s $2,938.44 more, but let’s be honest, that $3,000 per year difference in tuition is not the reason millennial home buying is allegedly harder than Boomer home buying.

The Take Away

After accounting for median house prices, inflation, interest rates, incomes, and debts; it’s pretty much just as hard for Millennials to purchase a home in today’s Puget Sound housing market as it was for our Boomer parents. So what’s the deal? There has to be a reason the narrative exists. Here’s my hypothesis: I think the biggest factor at play in this entire conversation of “Boomers had it easier than Millennials” is where the “Sticks” or suburbs begin. In 1980, I would imagine Wallingford was generally the outer perimeter of “Seattle,” and that’s where first-time homebuyers bought.

Today, with population growth, the outer perimeter of Seattle is probably closer to Shoreline(ish) to the North, and Burien(ish) to the South. Thus, the reason it’s harder for Millennials to purchase in “Seattle” than Boomers, is because the comparable Seattle neighborhoods the Boomers bought into are now an additional 7 miles north or south than they were in the 1980s, and Millennials just don’t define today’s comparable neighborhoods as “Seattle”. Otherwise, after taking into account the general growth of Seattle, it’s basically the same difficulty for first-time homebuyers today as it was for first-time homebuyers in the 1980s.

Alex Black Absorption Rates per NWMLS Real-Time Data

Absorption Rate is calculated as: (Pending Sales) / (Active + Pending Sales)

SFR in Seattle

- SFR Pending Sales in Seattle: 570

- SFR Active Listings in Seattle: 1,367 homes

- Absorption Rate for SFR in Seattle: 29.43%

- Buyer activity decreased in relation to seller activity this past week = slightly decreasing median SFR prices possible

Condos in Seattle

- Condo Pending Sales in Seattle: 229

- Condo Active Listings in Seattle: 684

- Absorption Rate for Condos in Seattle: 25.08%

- Buyer activity decreased slightly in relation to seller activity this past week = slightly decreasing median condo prices possible

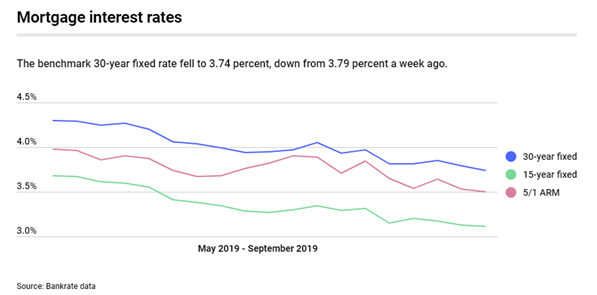

Interest Rates

Per Bankrate.com, the 30 year mortgage interest rate fell to 3.74%, with .30 in discount and origination points.

Rates have fallen 1.36% since their 52 week high of 5.1%

(That’s a savings of $402.01 per month on a $500,000 loan!)

Mortgage Rates

The benchmark 30-year fixed-rate mortgage fell this week to 3.74 percent from 3.79 percent, according to Bankrate’s weekly survey of large lenders. A year ago, it was 4.71 percent. Four weeks ago, the rate was 3.81 percent. The 30-year fixed-rate average for this week is 1.36 percentage points below the 52-week high of 5.10 percent, and matches the 52-week low of 3.74 percent.

The 30-year fixed mortgages in this week’s survey had an average total of 0.30 discount and origination points.

Over the past 52 weeks, the 30-year fixed has averaged 4.47 percent. This week’s rate is 0.73 percentage points lower than the 52-week average.

- The 15-year fixed-rate mortgage fell to 3.11 percent from 3.13 percent.

- The 5/1 adjustable-rate mortgage fell to 3.50 percent from 3.53 percent.

- The 30-year fixed-rate jumbo mortgage fell to 3.71 percent from 3.72 percent.

- At the current 30-year fixed rate, you’ll pay $462.55 each month for every $100,000 you borrow, down from $465.39 last week.

- At the current 15-year fixed rate, you’ll pay $695.88 each month for every $100,000 you borrow, down from $696.85 last week.

- At the current 5/1 ARM rate, you’ll pay $449.04 each month for every $100,000 you borrow, down from $450.72 last week.

The “Bankrate.com National Average,” or “national survey of large lenders,” is conducted weekly. The results of this survey are quoted in our weekly articles and national media outlets. To conduct the National Average survey, Bankrate obtains rate information from the 10 largest banks and thrifts in 10 large U.S. markets. In the Bankrate.com national survey, our Market Analysis team gathers rates and/or yields on banking deposits, loans and mortgages. We’ve conducted this survey in the same manner for more than 30 years, and because it’s consistently done the way it is, it gives an accurate national apples-to-apples comparison. https://www.bankrate.com/mortgages/analysis/

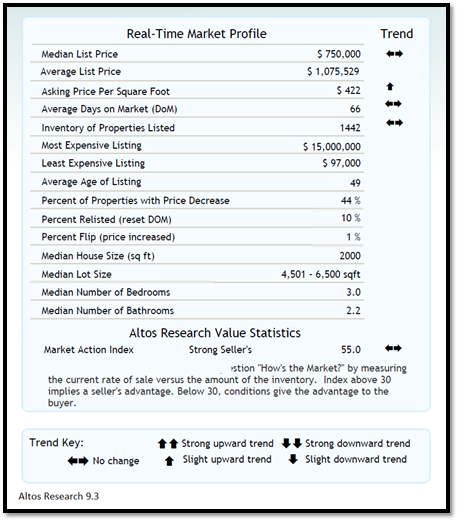

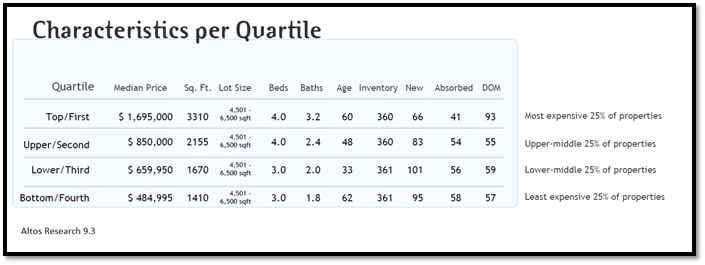

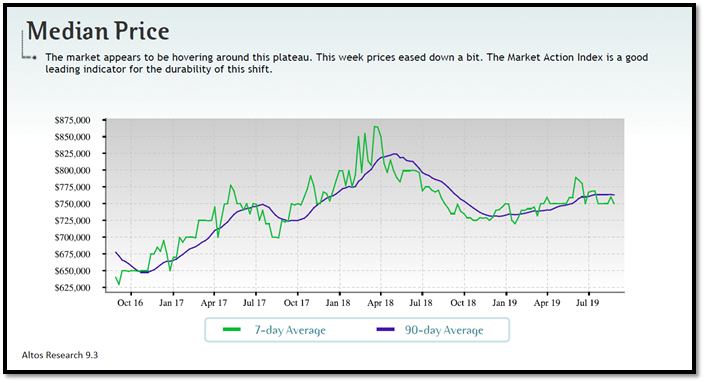

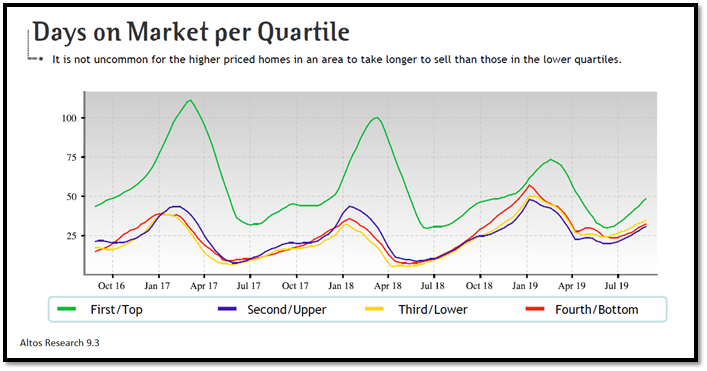

City of Seattle Stats for Single Family Residences – Updated 9.3.19

These charts are Seattle Specific, but the Puget Sound Real Estate Market mirrors the Seattle market.

Scott Sheridan is a Loan Officer with Primary Residential Mortgage, Inc. Being in the mortgage industry for three years, Scott brings a fresh millennial flair to the industry. He is well-versed in the most modern, efficient, and convenient ways to get things done. Scott combines these skills with a genuine love of his work and recent experience in what is it like to be a first and second-time home buyer. You can follow Scott’s weekly market updates on his PRMI

Be First to Comment