The conventional conforming loan limit is going from $484,350 to $510,400, and the conforming high balance limit is going from $726,525 to $741,750. What does this mean? Here’s the rundown:

For King, Pierce, and Snohomish Counties, the conforming loan limit is rising 2.09%. For all other counties in the state, the loan limit is rising 5.38%. The reason Fannie, Freddie, and Ginnie do this is to keep conforming loan limits relatively in line with housing market appreciation. This keeps buyer mortgage-eligibility in line with the local housing market’s median house price.

Technically, any loan above $510,400 is considered a jumbo loan. But because houses are so dang expensive in the Tri-County area, we get the opportunity to finance a home through Fannie, Freddie, and Ginnie all the way up to $741,750. This means most people whose loan amounts are below that ceiling will be able to take advantage of Fannie, Freddie, and Ginnie mortgage underwriting guidelines. This is important because those guidelines are much easier to meet than jumbo loan guidelines. This opens the door of homeownership possibility to more people in King, Pierce, and Snohomish Counties.

The biggest differences between Conforming loans and Jumbo loans are:

-

- Jumbo loans have a reserve requirement. This means they require that the buyer have additional liquid cash after buying the home. Generally, the liquid cash requirement is to the tune of $50,000 – $100,000. This is difficult because most people don’t have this after dropping their pretty penny on down payment and transaction costs.

- Jumbo loans require more down payment than conforming loans. Fannie and Freddie only require 5% down; and Ginnie only requires 3.5% down for an FHA loan, and 0% down for a VA loan.

- Jumbo loans have higher credit score requirements.

- Jumbo loans generally have higher interest rates compared to conforming loans unless putting 25%+ down.

- Jumbo loans oftentimes have tradeline requirements (Think: the borrower must have two credit cards and one installment loan, which have all been open for at least two years with perfect payment history).

In 2015 the conventional conforming loan limit was $417,000, and the conforming high balance loan limit was $517,500 for King/Pierce/Snohomish. In the last four years, the conventional conforming loan limit has risen 22.39% (+$93,400), and the high balance loan limit has risen 43.33% (+$224,250). These loan limit increases have supported the buyer pool, and its mortgage eligibility and purchasing power. This has helped support the Puget Sound Housing market.

Without these increases, the buyer pool would have been much dryer at the higher purchasing prices, and our housing market would not have appreciated like it has since 2015. Median home price in King County per the NWMLS in January 2015 was $390,000 – this is a combined number including Single-Family Residents and Condos. Today, that same metric has a median home price of $605,000 in King County. That’s a 55.13% appreciation growth rate over that timespan.

Summary

This isn’t necessarily front-page news, but this move is literally one of the top 3 supporting vertebrae in the Puget Sound Housing Market’s backbone. The other two most important vertebrae being the local job market and mortgage interest rates. These moves by the FHFA are invaluable to supporting our local housing market and clear the way for home prices to inch higher in 2020.

To read more about the loan limit increase, check out the Housingwire article here: https://www.housingwire.com/articles/fannie-mae-freddie-mac-loan-limit-increases-to-more-than-510000/

Alex Black Absorption Rates per NWMLS Real-Time Data

Absorption Rate is calculated as: (Pending Sales) / (Active + Pending Sales)

SFR in Seattle

- SFR Pending Sales in Seattle: 604

- SFR Active Listings in Seattle: 927 homes

- Absorption Rate for SFR in Seattle: 39.45%

- Buyer activity has increased relative to seller activity, meaning increasing prices are possible. On 9/6/19, the absorption rate was 29.43% for SFR in Seattle…aka, the SFR absorption rate has increased 34.05% since the beginning of September.

Condos in Seattle

- Condo Pending Sales in Seattle: 180

- Condo Active Listings in Seattle: 530

- Absorption Rate for Condos in Seattle: 25.35%

- Buyer activity has increased relative to seller activity, meaning slighting increasing condo prices are possible.

Interest Rates

This week’s survey has yet to be released, but if we’re crunching last week’s survey…Per Bankrate.com’s survey of large lenders, the 30 year mortgage interest rate fell to 3.89%, with .32 in discount and origination points.

According to Bankrate, rates have fallen 1.12% since their 52-week high of 5.01%

(That’s a savings of $331.68 per month on a $500,000 loan!)

Kyle’s Quick Take

Bankrate’s Survey of Large Lenders and their write up (below) is from last week… This week’s survey and rates haven’t been released yet. BUT FEAR NOT!!! I can tell you that the mortgage bond last Wednesday closed at 101.47, and right now it’s trading at 101.36. Thus, rates are SLIGHTLY higher than last week (as the price of the mortgage bond falls, mortgage interest rates rise). For context: This market movement lower has about the same impact on mortgage interest rates, as the impact on your 401k if the Dow Jones lost 75 points…It’s not in the direction we want it to go, but it’s sort of a negligible difference.

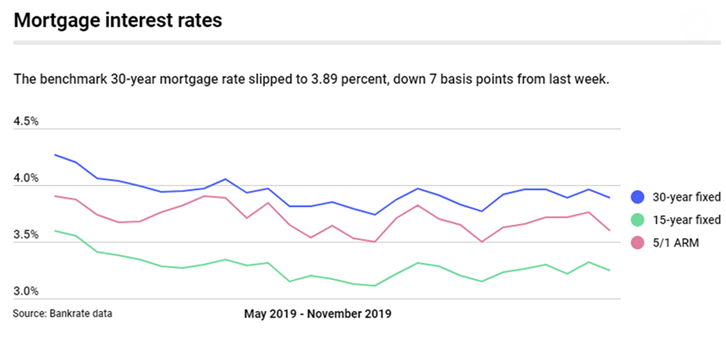

Mortgage rates this week

Mortgage rates fell 7 basis points this week, as Treasury yields pulled back, but that was no help for refinance activity, which has cooled in recent weeks.

The benchmark 30-year fixed-rate mortgage fell this week to 3.89 percent from 3.96 percent, according to Bankrate’s weekly survey of large lenders. A year ago, it was 5.01 percent. Four weeks ago, the rate was 3.96 percent. The 30-year fixed-rate average for this week is 1.12 percentage points below the 52-week high of 5.01 percent, and is 0.15 percentage points higher than the 52-week low of 3.74 percent.

Purchase applications get a boost as refinance activity declines

On the whole, mortgage applications fell by 2.2 percent from one week earlier, according to recent data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey. MBA’s results include an adjustment for the Veterans Day holiday.

The purchase application share, however, rose by 7 percent from last week, which is 152 percent higher than this time last year. This might be a sign that the much-needed expansion in housing inventory is starting to materialize, says Joel Kan, MBA’s vice president of economic and industry forecasting.

Refinance activity, on the other hand, is dragging application volume down, even as rates stay below 4 percent. Last week, refinance activity fell by 8 percent, according to the MBA survey.

“Despite lower rates, mortgage applications decreased 2.2 percent, driven by an 8 percent slide in refinance activity,” Kan says. “Rates have stayed in the same narrow range of around 4 percent since July, so we may be starting to see the expected slowdown in refinancing as the pool of eligible homeowners shrinks.”

Mortgage rates this week

The 30-year fixed mortgages in this week’s survey had an average total of 0.32 discount and origination points.

Over the past 52 weeks, the 30-year fixed has averaged 4.22 percent. This week’s rate is 0.33 percentage points lower than the 52-week average.

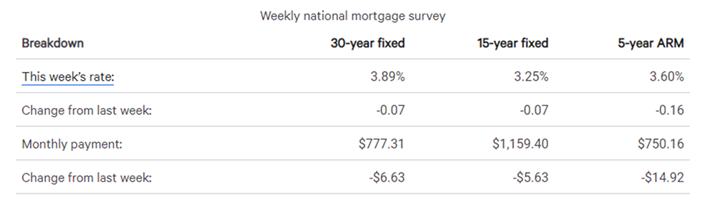

- The 15-year fixed-rate mortgage fell to 3.25 percent from 3.32 percent.

- The 5/1 adjustable-rate mortgage fell to 3.60 percent from 3.76 percent.

- The 30-year fixed-rate jumbo mortgage fell to 3.77 percent from 3.85 percent.

- At the current 30-year fixed rate, you’ll pay $471.10 each month for every $100,000 you borrow, down from $475.11 last week.

- At the current 15-year fixed rate, you’ll pay $702.67 each month for every $100,000 you borrow, down from $706.08 last week.

- At the current 5/1 ARM rate, you’ll pay $454.65 each month for every $100,000 you borrow, down from $463.68 last week.

Results of Bankrate.com’s weekly national survey of large lenders conducted November 20, 2019 and the effect on monthly payments for a $165,000 loan:

The “Bankrate.com National Average,” or “national survey of large lenders,” is conducted weekly. The results of this survey are quoted in our weekly articles and national media outlets. To conduct the National Average survey, Bankrate obtains rate information from the 10 largest banks and thrifts in 10 large U.S. markets. In the Bankrate.com national survey, our Market Analysis team gathers rates and/or yields on banking deposits, loans, and mortgages. We’ve conducted this survey in the same manner for more than 30 years, and because it’s consistently done the way it is, it gives an accurate national apples-to-apples comparison. https://www.bankrate.com/mortgages/analysis/

Scott Sheridan is a Loan Officer with Primary Residential Mortgage, Inc. Being in the mortgage industry for four years, Scott brings a fresh millennial flair to the industry. He is well-versed in the most modern, efficient, and convenient ways to get things done. Scott combines these skills with a genuine love of his work and recent experience in what is it like to be a first and second-time home buyer.

Be First to Comment